Loan interest can seem like a daunting concept, but understanding how it works is crucial for making informed financial decisions. Whether you’re considering a car loan, mortgage, or personal loan, knowing how to calculate interest will help you determine the true cost of borrowing. Let’s break down some easy ways to get a handle on those numbers.

Why Understanding Loan Interest Matters

Before diving into calculations, let’s emphasize why this knowledge is so important:

- Accurate Budgeting: Knowing the total interest you’ll pay allows you to create a realistic budget and avoid financial surprises.

- Comparing Loan Offers: Understanding interest rates and how they affect your payments enables you to compare different loan offers and choose the best deal.

- Financial Awareness: Being aware of how interest works empowers you to make informed decisions about your finances and avoid unnecessary debt.

Simple Interest vs. Compound Interest

First, it’s vital to know the difference between simple and compound interest:

- Simple Interest: Calculated only on the principal amount (the original loan amount).

- Compound Interest: Calculated on the principal amount and the accumulated interest from previous periods. This is the more common type with loans.

Most loans, like mortgages and car loans, use compound interest. Therefore, we will focus on this.

Easy Ways to Calculate Loan Interest:

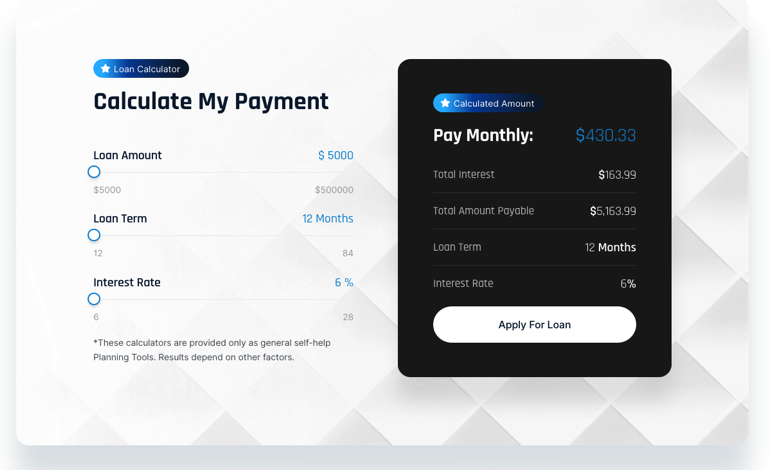

- Online Loan Calculators:

- The easiest and most convenient way to calculate loan interest is by using online loan calculators.

- The loan calculator available on our homepage.

- Simply enter the loan amount, interest rate, and loan term, and the calculator will provide you with the monthly payment, total interest paid, and amortization schedule.

- These tools are very useful for “what if” scenarios, where you change the loan amount, interest rate, or loan term to see the affect.

- Amortization Schedule:

- An amortization schedule is a table that shows the breakdown of each loan payment, including the amount that goes toward principal and the amount that goes toward interest.

- Many lenders provide an amortization schedule when you take out a loan.

- You can also find online tools that generate amortization schedules.

- By looking at the schedule, you can see how much interest you’re paying with each payment.

- Basic Formula (Approximation):

- While compound interest calculations can be complex, you can get a rough estimate using a simplified approach.

- For a general idea, you can multiply the loan amount by the interest rate, and then by the length of the loan. This will give you a rough estimate of the intrest paid. This will not be perfectly accurate, but will be a good starting point.

- This is a simplified way to get a general idea, and is not a replacement for a proper amortization schedule.

Tips for Minimizing Loan Interest:

Shop Around for the Best Rates: Compare loan offers from multiple lenders to find the most favorable terms. inventore veritatis et quasi architecto beatae vitae dicta sunt explicabo. Aelltes port lacus quis enim var sed efficitur turpis gilla sed sit amet finibus eros. Lorem Ipsum is simply dummy text of the printing.

Improve Your Credit Score: A higher credit score can qualify you for lower interest rates.

Make Larger Down Payments: Reducing the loan amount will decrease the total interest paid.

Shorten the Loan Term: While monthly payments will be higher, you’ll pay less interest overall.

Calculating loan interest doesn’t have to be intimidating. By utilizing online calculators, understanding amortization schedules, and following these tips, you can gain a clear understanding of your loan costs and make informed financial decisions.